Welcome! AsianBondsOnline is a one-stop source of information on bond markets in emerging East Asia.

This detailed guidance has been created to assist bond issuers and their advisors to understand the process and key considerations for a successful green bond issuance.

Demand for green bonds and other sustainable finance products is increasing rapidly. Issuers are seeing an opportunity to be part of the green bond market, but are often not sure about how it works, what they need to do, and the key decisions to be made along the way.

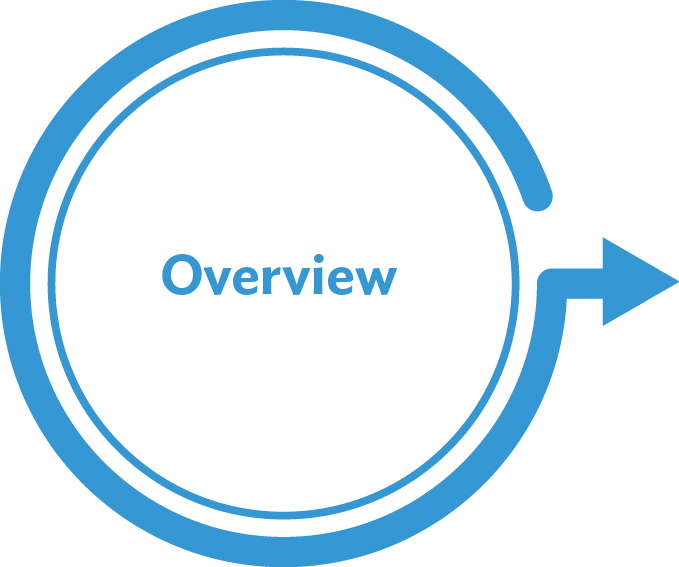

The section covers all of the steps required to follow best practices in labeling bonds. They include relevant examples, links to further details, and key resources for green bond issuers and their deal teams.

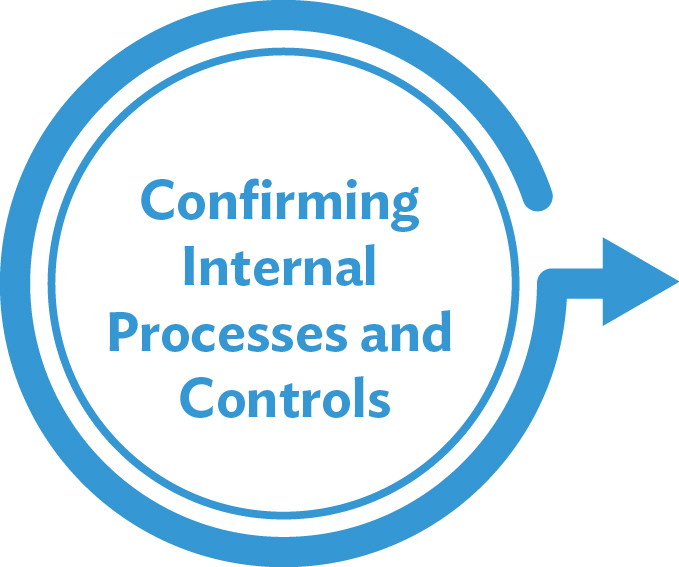

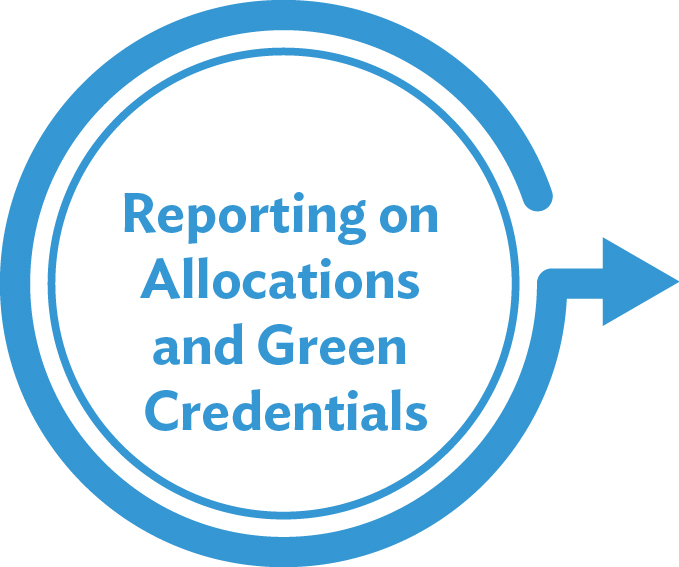

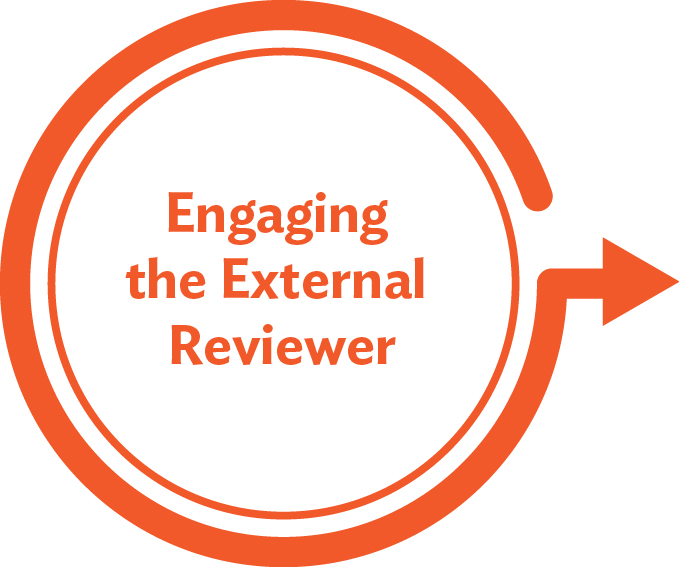

Outline of the Labeling Process

Source: Authors’ illustration.

There is often confusion among issuers and advisors on the differences between a sustainability bond and a sustainability-linked bond. It is important to make clarification on the use-of-proceeds model compared to sustainability-linked arrangements, as this guidance note only covers the use-of-proceeds model.

There are currently two major approaches to identifying bonds and debt instruments as having positive green or sustainability value. Green bonds, climate bonds, social bonds, and sustainability bonds all rely on the use-of-proceeds approach. This is the most common approach used by bond issuers. It identifies specific green projects and assets that are associated with the green bond.

Recently, there has been a surge in the alternative approach, which links sustainability outcomes for the bond issuer to the amount of interest (coupon rate) that is paid to investors. This usually involves a step-up or step-down in coupon rates triggered by the achievement (or not) of specific sustainability targets.

- Use-of-proceeds approach. Per the Green Bond Principles, this refers to “any type of bond instrument where the proceeds will be exclusively applied to finance or re-finance, in part or in full, new and/or existing eligible green projects and assets, and which are aligned with the four core components of the Green Bond Principles.”

- Sustainability-linked approach. Per the Sustainability-Linked Bond Principles, this refers to “any type of bond instrument for which the financial and/or structural characteristics can vary depending on whether the issuer achieves predefined sustainability or [environmental, social, or governance] objectives. In that sense, issuers are thereby committing explicitly (including in the bond documentation) to future improvements in sustainability outcome(s) within a predefined timeline. [Sustainability-Linked Bonds] are a forward-looking, performance-based instrument and are aligned with the Sustainability-Linked Bond Principles.”

Two Parallel Tracks

There are two tracks of work to consider when labeling a bond, loan, or sukuk (Islamic bond) as “green.” These two tracks are equally important to investors when they are considering the labeled investment.

The first track is for the eligibility of the projects and assets. This involves the issuer demonstrating that the projects and assets associated with the green bond are aligned with a set of green definitions, or a “taxonomy.” Selecting which taxonomy to use, or when not to use one, is described in Factsheet #2.

The second track is for the integrity of the issuer’s internal systems and controls when it comes to the processes involved in labeling a bond. This includes procedures and governance for selecting green projects and assets, management of the bond proceeds, and regular reporting and disclosure in line with the issuer’s Green Bond Framework.

The guidance in these factsheets highlights best practices for both of the abovementioned tracks. Issuers can achieve best practices in the second track of work, no matter which green definitions are used. These internal systems and controls can support a broad range of labeling activities for an issuer (e.g., green, social, or sustainable).

The First Time Is Challenging but Worth It

Issuers of green bonds have described the extra effort required for labeling as being much higher for the first labeled transaction but much less for future activities. Subsequent green transactions use the same Green Bond Framework, internal processes, and controls and tracking of proceeds as for the first green transaction, so it is much easier and faster compared to the first time.

Treasurers from green bond issuers have described their strong intention to issue further green and labeled debt instruments, even though there was extra effort required to label the first transaction.

There are substantial benefits for green bond issuers if they can be the first to issue a green bond in a particular jurisdiction or a new sector, or by using a new structure. This amplifies the potential for the green bond to provide positive momentum for the issuer’s sustainability credentials.

“BTSG’s 2nd series of Green Bond issued in November 2020 with 3.3x oversubscription indicated investors’ confidence and goodwill towards the company and our green projects. On back of strong demand, BTSG decided to exercise the THB 3,600 million greenshoe option bringing total issue size to THB 8,600 million. The proceed will be used to fund two new monorail projects (Pink line : 34.5 kms , Yellow line : 30.5 kms) in Bangkok which target to operate during 2021-2022. Both are the anchored projects that will elevate Bangkok’s electric mass transit network which will lessen the use of fossil-fueled vehicles resulting in the reduction of carbon emissions and fine dust particles (PM2.5) in Bangkok metropolitan area. It is estimated that both projects will help reduce CO2 emission by 28,000 tons per year and will play an important role in bringing cleaner air quality to the city. Although issuing Green Bond require additional work and resources to comply with Green Bond framework , we felt it is worthwhile. It is also worth mentioning that since this is our 2nd issuance, our team had quite a steep learning curve and able to work much faster.”

K.Surayut Thavikulwat

Chief Financial Officer

BTS Group Holdings PCL